- Smart Contract

- Payment

- DeFi

- Inter-Blockchain Communication

- Centralized Exchange

- Money Infrastructure

- Specialized Utility

- Community

- Gimmick

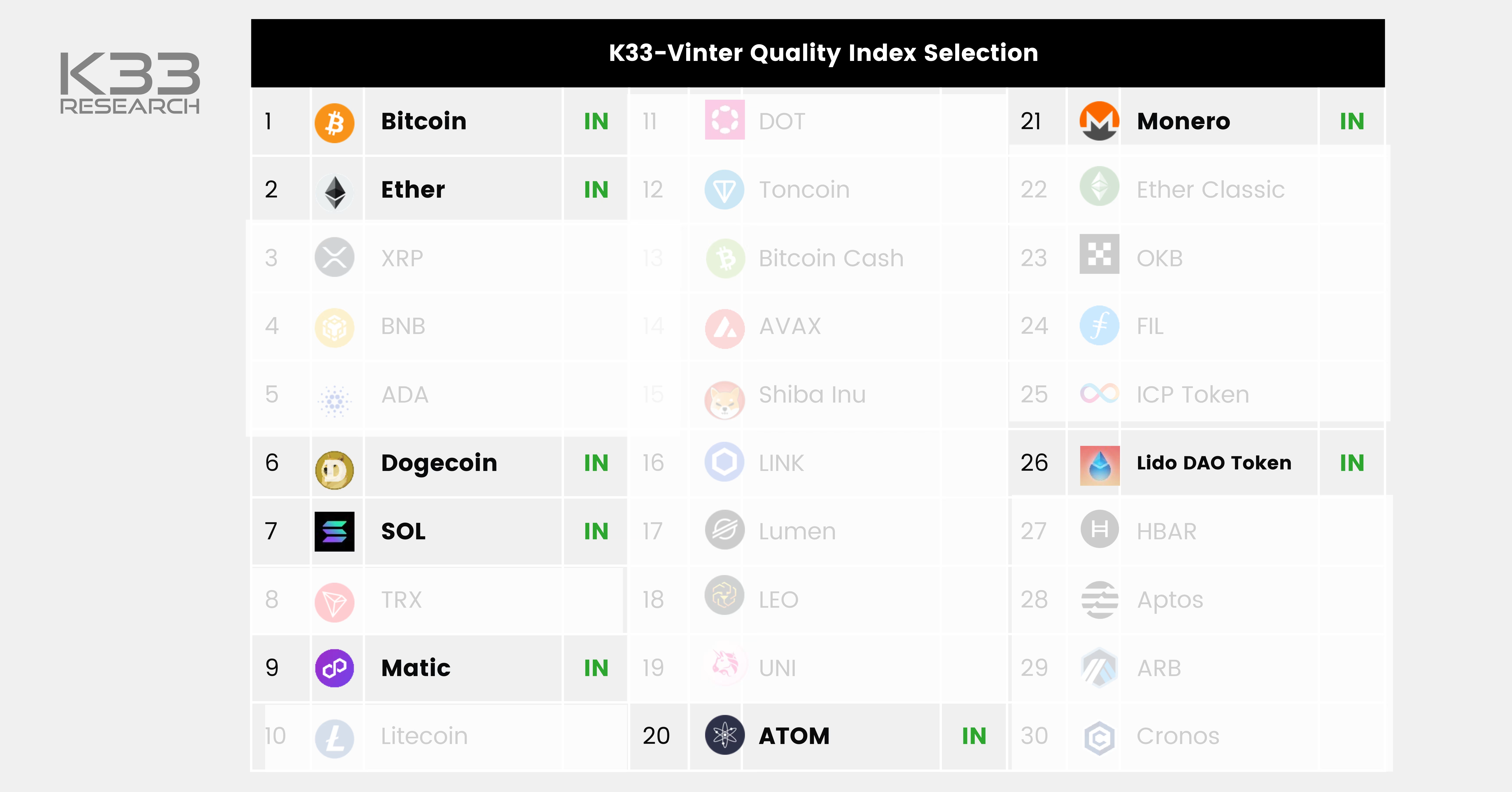

Methodology - The K33 Vinter Quality Index

The KVQ index comprises an equally weighted mix of the most promising tokens amongst the top 30 crypto assets. Tokens with a low long term survival-probability are excluded, contributing to a substantial reduction in downside risk in the index.Preview

A top 30 token must pass the Quality Filter for inclusion in the index. The purpose of the Quality Filter is to evaluate the quality of crypto assets from an investor's standpoint. A high-quality asset is defined as an asset with a small probability of permanent financial loss, while a low-quality asset possesses a significant probability of permanent financial loss. The quality filter consists of the following four steps. 1. Categorize: Each asset is assigned to a category, which allows for relative comparison.2. Exclude: Assets with faulty tokenomics, missing information, or presenting a lack of transparency are taken out.3. Evaluate: Five pillars enable the evaluation of an asset's quality for each category. 4. Rank: The Quality Filter selects the highest-ranked assets with scores above the cutoff Quality Score.The quality filter must include subjective analysisThe selection assessments should not be considered a universal truth, and others could provide compelling adverse arguments to our selections. Contrary to traditional finance, all the "bank" 's data are there for all to see in crypto. However, in most cases, you won't know, in the strictest sense, whose data or what you are looking at. By looking at the blockchain data itself, it's impossible to evaluate what's "real" volume or "fake" volume, whether 1000 addresses are really just one guy or a thousand, etc. To make sense of the blockchain data, you must therefore make inferences from outside knowledge in combination with what the blockchain tells you. To assess whether a token should be included in the "K33 Vinter Quality Index," we use a combination of standardized metrics and our specialist knowledge.A good stock portfolio will not, by definition, include good companies but rather good investments, i.e., companies with a low price compared to the fair price. Crypto markets are still immature, and at the current time, there are no well-established pricing models like the discounted cash flow model in traditional valuation of stocks. We believe many tokens' prices will eventually go close to zero. At the moment, the K33 Vinter Quality Index is mainly about excluding the tokens with a low probability of keeping value long-term. As our work on- and understanding of token prices expand, the index will be updated accordingly.The Quality Filter1. CategoriesCategories regroup and enable the comparison of assets having similar purposes. Each asset in the top 30 by market capitalization belongs to one of these categories: